Latest Post

Samsung Galaxy S25 5G

Top 10 Upcoming Tech Gadgets to Watch Out for in 2...

Yamaha R7 2025: Redefining Performance for Indian...

Yamaha R7 2025: Price & Specs

Yamaha R7 2025: The Bike That’s Set to Redefine Pe...

Why the Yamaha R7 2025 is a Game-Changer for Super...

Yamaha R7 2025: The Supersport Ready to Dominate I...

2025 VW Golf GTI: The Hot Hatch Everyone Wants

Why the 2025 VW Golf GTI Remains the Ultimate Hot...

Volkswagen Golf GTI Launch Date & Price in India

How to Earn Money Online in India for 2025 Success

How to Fix Unresponsive iPhone Touchscreen Fast

How to Unlock HP Touchpad on Laptop Quick Fixes

How to Set Up USB Tethering on Windows 11 Step by...

How to Fix a Faulty Keyboard Key Fast

How to Install a Second SSD in Your PC Fast

How to Fix 'No Battery Detected' Error Fast

Google Assistant 2025: Step-by-Step Guide to Turn...

Alexa Whisper Mode 2025: Step-by-Step Guide to Ena...

Google Home Setup 2025: Step-by-Step Guide for Eas...

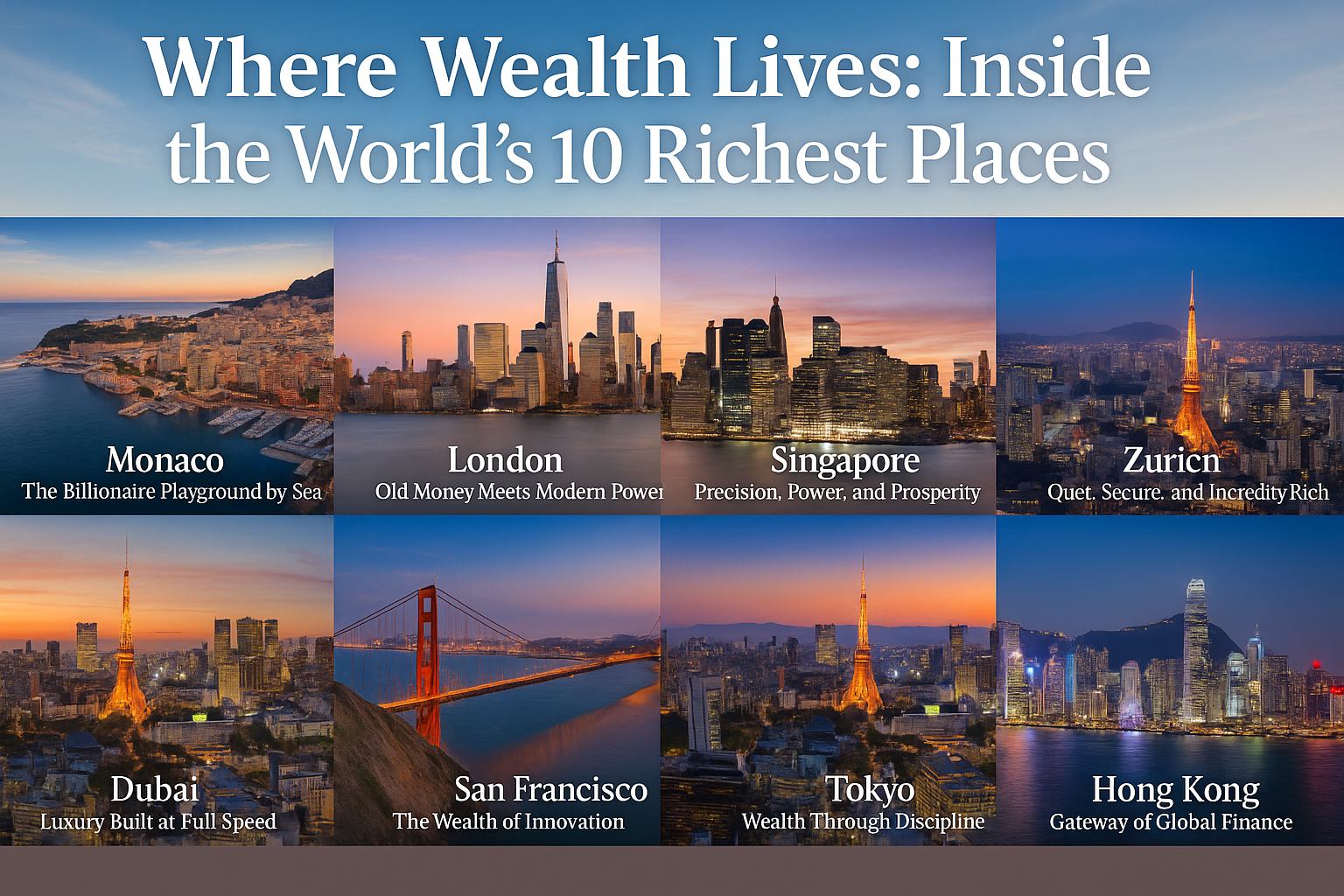

Worlds 10 Richest Places Where Global Wealth Lives

India Top 10 Richest People in 2025

The Billion Dollar Minds Worlds Top 10 Richest Per...

Meesho IPO Debut: Market Sentiment Mixed as GMP Ea...

Indian Markets Open Lower Amid Fresh Tariff Concer...

Sensex tanks 800 points, Nifty slips under 25,900...

Meesho IPO Allocation and Market Launch

ICICI Prudential AMC Prepares for IPO: RHP Filing...

Grow Mutual Fund Unveils Nifty Metal ETF

2025 Personal Loan RBI Update TN Kerala Salaried

Retirement Planning India How Much Save Invest Tim...

Digital Payments Security Protect Money on UPI Wal...

Aries Daily Horoscope 17 Dec 2025

Pisces Daily Horoscope 15 Dec 2025

Aquarius Daily Horoscope 15 Dec 2025

Capricorn Daily Horoscope 15 Dec 2025

Sagittarius Daily Horoscope 15 Dec 2025

Scorpio Daily Horoscope 15 Dec 2025

Libra Daily Horoscope 15 Dec 2025

Virgo Daily Horoscope 15 Dec 2025

Leo Daily Horoscope 15 Dec 2025

Cancer 15 Dec 2025

Home Gym Setup Under 25000 Equipment Space and Bud...

Skin Fitness Daily Habits for Radiant Skin Beyond...

Mindful Eating Guide How to Stop Overeating and Im...

10 Minute Standing Desk Workout for Office Workers...

Intermittent Fasting for Women in India Diet Benef...

10 Minute Daily Workout Plan for Busy People Home...

Morning Drinks for Weight Loss and Glowing Skin Ay...

How to Fix Sleep Schedule Naturally with Proven Ti...

Best Vegetarian Protein Sources in India for Gym a...

Intermittent Fasting for Beginners with Indian Mea...

How to Build Stamina and Strength Naturally Indian...

Foods to Avoid for Weight Loss Indian Diet Mistake...